Most transaction monitoring systems are built to look busy. Hundreds of alerts. Overnight batch runs. Static thresholds set once and never touched. They generate the appearance of compliance – and leave the actual gaps wide open.

Transaction monitoring means continuous financial activity screening – payments, customer events, behavioral patterns. Its goal is to detect money laundering, fraud, and sanctions violations before they become regulatory failures.

Done precisely, it gives compliance teams real control.

Done poorly, it just fills inboxes.

What transaction monitoring actually covers

A complete system covers more than payments. It includes:

- Payment flows – individual transfers, aggregated volumes, velocity patterns, and cross-border activity

- Customer events – onboarding changes, profile updates, and behavioral shifts that alter risk level mid-relationship

- Sanctions screening – continuous matching against OFAC (Office of Foreign Assets Control), EU, UN, and national watchlists at the point of transaction or customer event

- PEP (Politically Exposed Person) monitoring – real-time detection when a customer becomes a politically exposed person, not just at onboarding

- Adverse media – ongoing screening that reflects the current state of the world, not last quarter's data

If yours only watches payments, it has structural gaps. Financial crime doesn't confine itself to a single data type.

It also sits at the core of every AML (anti-money laundering) framework and is a regulatory requirement under FATF (Financial Action Task Force), FinCEN (Financial Crimes Enforcement Network), and EU AMLD (Anti-Money Laundering Directive) directives in the US, UK, and the EU.

Why real-time transaction monitoring is now the baseline

Every second your monitoring isn't running, risk accumulates. A suspicious transfer clears. A sanctioned counterparty slips through. A high-risk customer changes behavior – and nobody notices until it's too late.

Real-time transaction monitoring is no longer a competitive advantage. It's the required baseline.

Batch processing and overnight reviews create predictable blind spots. Sophisticated financial crime finds them. The question isn't whether to monitor in real time – it's whether your setup is precise enough to act on what it surfaces.

The real problem: inflexible tools, not complexity

Complexity is manageable. Compliance professionals are trained to see through regulatory mazes. The hard part of your job: finding flexible, but tools.

The most common issue in transaction monitoring is misaligned rules. They just keep hitting results, generating hundreds of low-quality alerts per day – even when tuning has not been done.

So analysts stop trusting the system. Alert fatigue sets in. Real risks get buried under noise. And it's its own compliance failure.

Compliance teams need tools that are both flexible and precise. Teams face constantly changing risks. A new fraud pattern. Changing regulations. Shifting customer behavior.

So compliance must stay aware and adapt. Their transaction monitoring cannot stay the same. A still system is a dead system – unable to identify and tackle new risks. Transaction monitoring tools must be easy to modify and fine tune at any given moment. Compliance cannot wait for IT or vendors to make time for small adjustments in code.

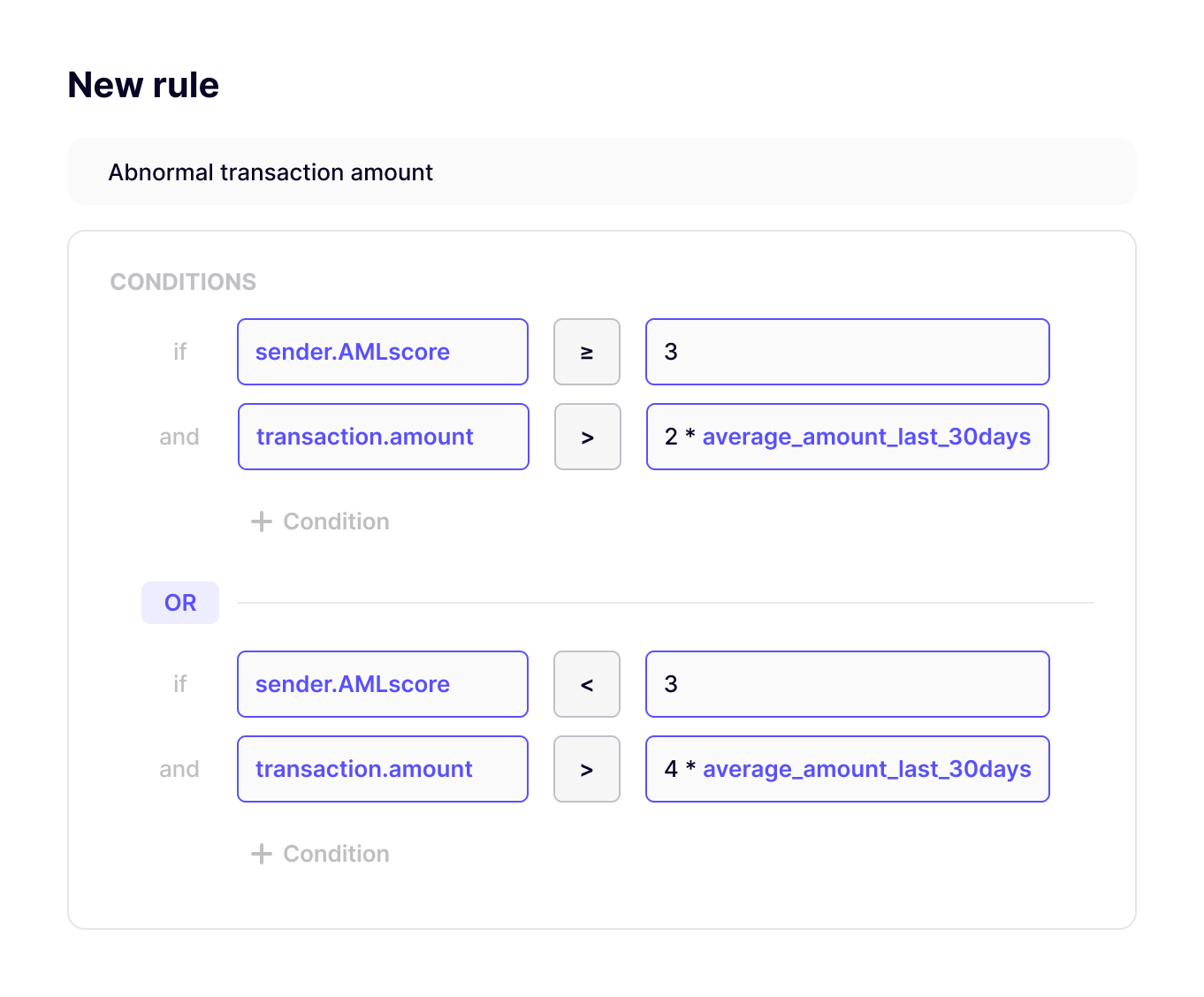

At the same time, the need for precise rules remains clear. Precision requires rules segmented by customer type, channel, product, and jurisdiction – not blanket logic that treats every transaction the same. It requires thresholds reviewed on a regular cycle, and matching logic that handles transliterations, aliases, and fuzzy matches without flooding your team with false hits.

Performance tuning isn't an IT task. It's a compliance discipline. Track alert-to-case conversion rates. Retire rules that fire constantly but never produce a real investigation.

Your monitoring system must get sharper and sharper over time – not stagnate.

Transaction monitoring best practices

High-performing compliance teams follow a consistent pattern.

- Write granular, segment-specific rules

A blanket rule covering all transactions fits nothing precisely. Segment by customer risk tier, transaction channel, product type, and geography. The more specific the rule, the more meaningful the alert. - Tune thresholds on a regular cycle

What was correctly calibrated six months ago may now be generating noise or missing new typologies. Set a formal review cadence – quarterly at minimum – and document every change. - Run recurring checks, not one-time screening

Onboarding screening alone isn't a monitoring program. Customers change. Sanctions lists change. PEP status changes. Your checks must keep pace with a customer's evolving risk profile throughout the relationship. - Maintain list freshness as a documented process

An outdated sanctions or PEP list isn't a safety net. It's a liability. Automate updates and document the chain. Regulators will ask. - Track rule performance, not just alert volume

Alert volume is a vanity metric. What matters is how many alerts convert to genuine investigations. A rule that fires constantly but never produces a case is generating cost, not compliance.

How Marble brings transaction monitoring into focus

Marble is built for compliance teams that won't accept the trade-off between speed, precision, and control.

The no-code rule builder lets you define monitoring logic that matches your business – by customer segment, transaction type, jurisdiction, or risk score. No vendor templates. No IT dependencies. The rules fit your framework, not the other way around.

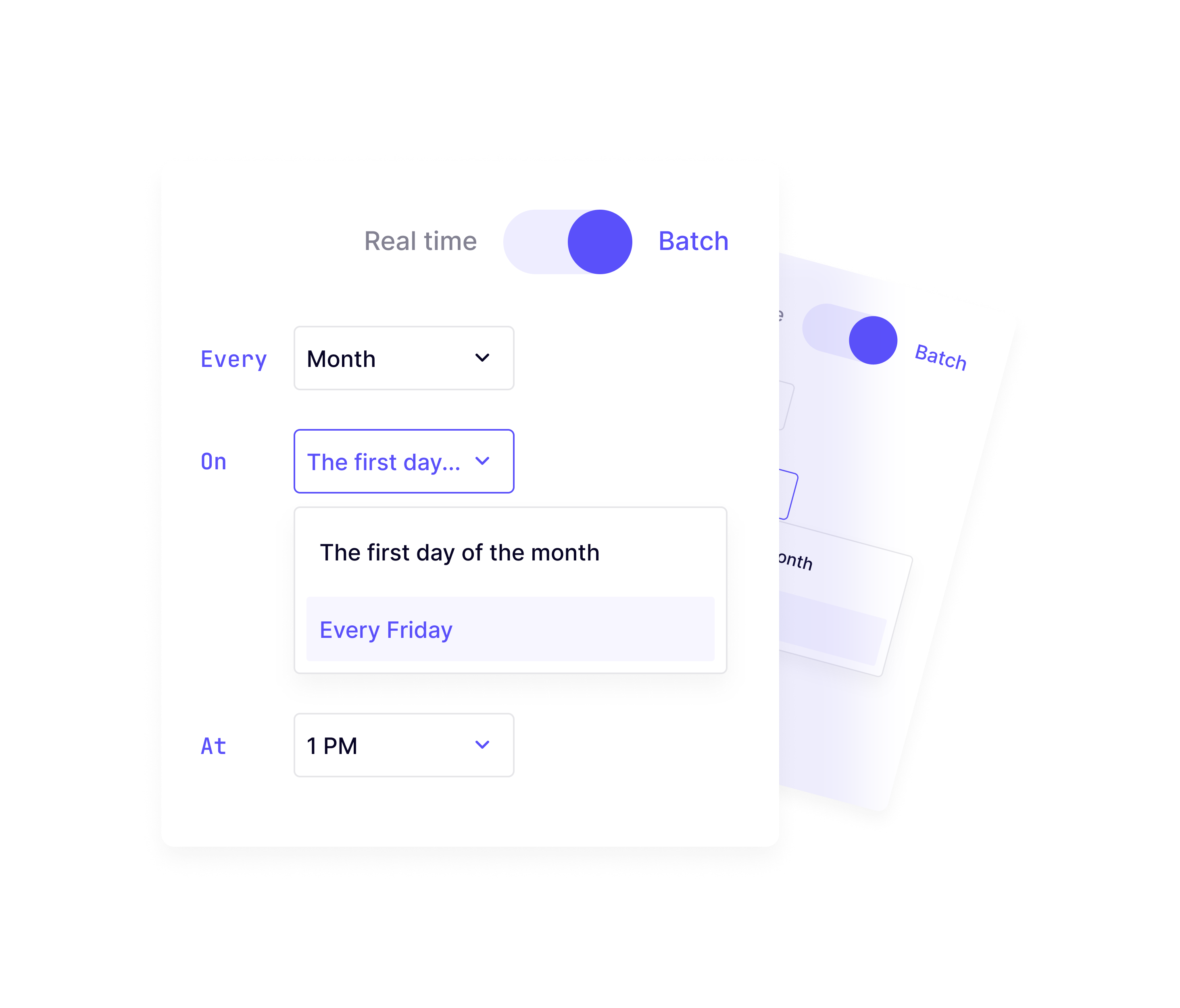

Run checks in real time at the moment of payment, or schedule them across your full customer portfolio.

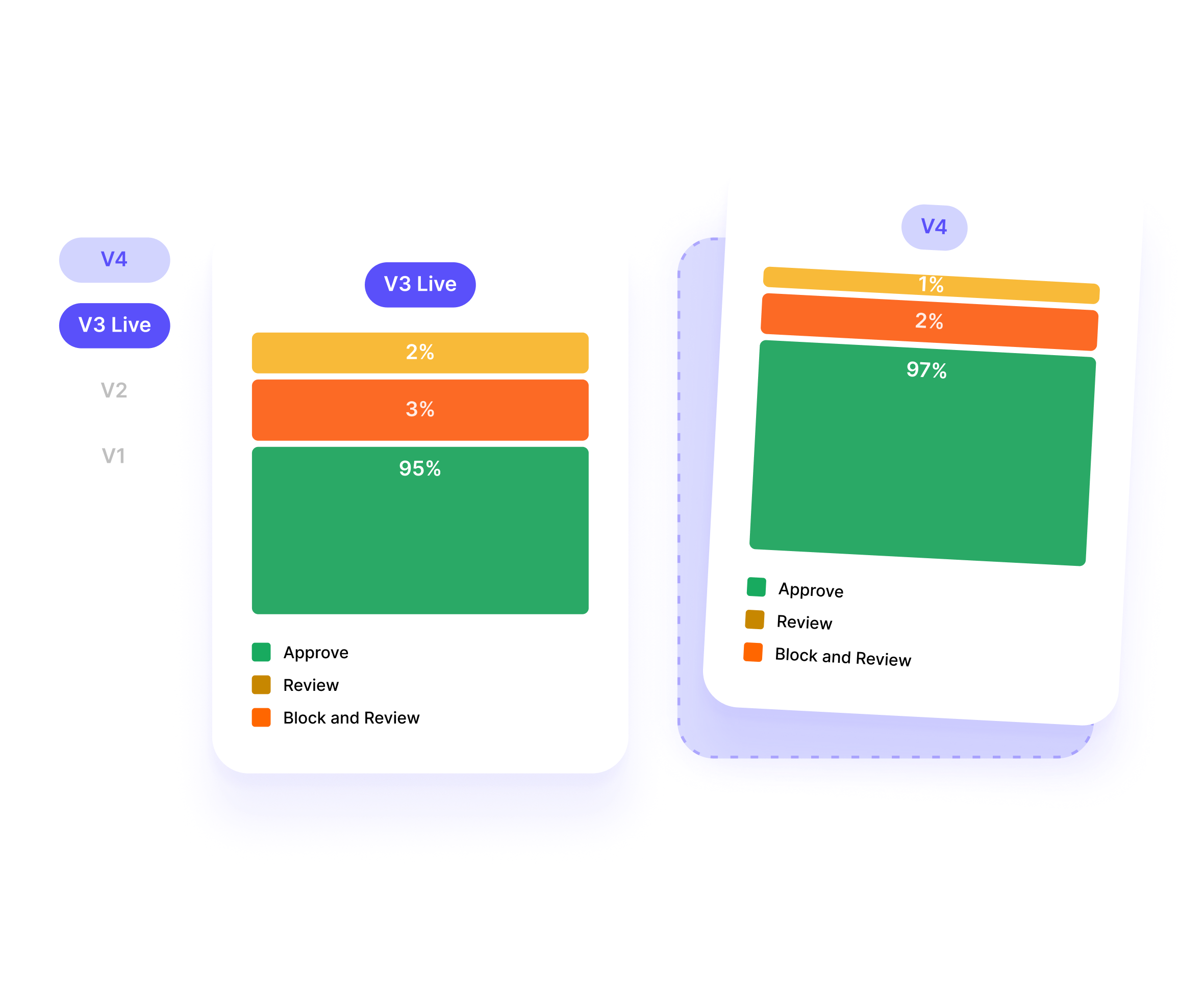

A/B test rule configurations against live data before promoting to production – so changes are made with evidence, not guesswork. And every alert, decision, and rule change is logged in a complete, regulator-ready audit trail.

Everything falls into place. Precisely.

Refine your transaction monitoring setup with Marble →

Frequently asked questions about transaction monitoring

What triggers a transaction monitoring alert?

Alerts fire when a transaction or customer event matches a defined rule: a payment exceeding a threshold, unusual velocity, a cross-border transfer to a high-risk jurisdiction, or a sanctions list name match.

Alert quality depends entirely on how well the rule is calibrated.

What is the difference between real-time and batch transaction monitoring?

Real-time monitoring screens each event as it occurs. Batch monitoring collects transactions over a period and analyses them together – creating gaps that can be exploited. Real-time prevents suspicious transactions from clearing unreviewed.

How do you reduce false positives in transaction monitoring?

Move from broad rules to segment-specific logic with regularly tuned thresholds. Smart matching – fuzzy logic, alias detection, transliteration handling – cuts noise. Regular rule performance reviews retire rules that generate alerts without producing investigations.

What regulations require transaction monitoring?

The most important regulations include:

- The BSA (Bank Secrecy Act) and FinCEN in the US

- EU AMLD

- the UK Proceeds of Crime Act and FCA (Financial Conduct Authority) guidance

- Globally: FATF Recommendations

What should a transaction monitoring audit trail include?

Every alert generated, every decision made, the rules and thresholds in force at the time, rule changes and their rationale, and the responsible compliance officer. Regulators expect to reconstruct your full decision-making process from the record alone.